Oswal Pumps Business Analysis

A Deep Dive into Oswal Pumps as it approaches listing in Indian Stock Market

1. Introduction of the Company

Oswal Pumps Limited (OPL) stands as a prominent vertically integrated manufacturer in the Indian market, specializing in a comprehensive range of pumping solutions and related technologies. The company’s core business encompasses solar-powered and grid-connected submersible and monoblock pumps, electric motors (including induction and submersible types), and solar modules, all marketed under its well-recognized 'Oswal' brand.

With over 21 years of experience in pump engineering, product design, manufacturing, and rigorous testing, OPL has cultivated a deep understanding of its industry. This extensive experience enables the company to address the diverse requirements of end-users across critical sectors such as agriculture, residential, and industrial applications. The operational backbone of OPL comprises two strategically located manufacturing facilities in Karnal, Haryana, with one dedicated to the production of pumps and motors, and the other focused on solar module manufacturing.

Oswal Pumps has established itself as a significant player in the solar pump segment, notably emerging as one of the largest suppliers of agri-solar pumps under the Indian government’s Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan Scheme ("PM Kusum Scheme").

This strategic positioning highlights the company's ability to leverage government initiatives and capture substantial market share in a rapidly expanding sector. The 'Oswal' brand has achieved positive market recognition, a testament to the company's consistent emphasis on product quality and effective brand-building initiatives throughout its operational history.

Furthermore, OPL's commitment to maintaining high standards is evidenced by its ISO 9001:2015, ISO 45001:2018, and ISO 14001:2015 certifications for both manufacturing facilities, ensuring adherence to international quality, environmental, and occupational health and safety standards. The company's inclusion in the Approved List of Manufacturers and Models (ALMM) for solar modules by the Ministry of New and Renewable Energy, Government of India, further validates its product quality and manufacturing capabilities.

The significant revenue contribution from the PM Kusum Scheme, which accounted for 85.72% of OPL's revenue from operations in Fiscal Year 2024, up from 55.32% in Fiscal Year 2022, is a critical observation. This substantial reliance on a government initiative indicates a deep strategic alignment with a national priority focused on energy security for farmers, reduction of diesel consumption, and promotion of renewable energy in the agricultural sector. This alignment has provided a strong demand tailwind, allowing OPL to position itself at the forefront of this governmental push and gain a significant competitive advantage in securing large-scale, subsidized projects. However, this high dependence on a government scheme, which is currently slated to expire in December 2026, introduces a considerable future risk. The company's ability to either diversify its revenue streams or ensure the extension of the scheme will be paramount. This situation underscores the importance of the company's stated strategies to expand into other states and directly sell to farmers, as these efforts are crucial for mitigating this concentration risk and ensuring long-term stability.

2. Detailed Business Explanation and Verticals

Oswal Pumps Limited operates with a comprehensive product portfolio and a well-defined operational structure that spans manufacturing, distribution, and service delivery across various end-use sectors.

Comprehensive Product Portfolio

Oswal Pumps manufactures a diverse range of products under the 'Oswal' brand, designed to cater to a wide array of applications. The product categories include:

Pumps: This segment comprises both solar-powered and grid-connected pumps. Solar submersible pumps are offered in a power range of 1 HP to 25 HP, while solar monoblock pumps are available from 3 HP to 20 HP. For grid-connected applications, submersible pumps range from 0.5 HP to 40 HP, and monoblock pumps from 0.5 HP to 15 HP.

Electric Motors: The company produces induction motors with a power range of 0.5 HP to 75 HP and submersible motors ranging from 0.5 HP to 150 HP.

Solar Modules: Manufactured through its wholly-owned subsidiary, Oswal Solar Structure Private Limited, these modules are an integral component for Turnkey Solar Pumping Systems, reflecting the company's backward integration strategy.

Analysis of Diverse Revenue Streams

The company's revenue is primaril generated from the sale of manufactured goods, encompassing both domestic and export markets, the sale of traded goods, and the provision of services, particularly the installation and commissioning of solar pumps. Additional operating revenue sources include export incentives and the sale of scrap materials.

The evolution of OPL's revenue streams over the past three fiscal years highlights a significant strategic shift:

In-depth Look at End-Use Sectors and Product Mix

OPL's products serve a variety of end-use applications, with a pronounced focus on the agricultural sector.

The product mix has undergone a significant transformation, demonstrating a strategic pivot towards Turnkey Solar Pumping Systems (TSPS). This shift is evident in the dramatic increase in revenue contribution from TSPS, while the share of standalone solar submersible pumps and non-solar pumps has decreased.

This shift from component/product supply to a comprehensive EPC (Engineering, Procurement, and Construction) player for solar pumping solutions is a fundamental strategic pivot. In Fiscal Year 2022, standalone Solar Submersible Pumps constituted nearly 50% of revenue, while TSPS (Submersible) was a mere 3.91%. By Fiscal Year 2024, TSPS (Submersible) alone commanded almost half of the revenue (49.49%), with TSPS (Monoblock) contributing an additional 11.56%.

This transformation allows Oswal Pumps to capture a larger portion of the value chain, as evidenced by the substantial increase in revenue from "Sale of services" (installation and commissioning of solar pumps) from ₹81.62 million in Fiscal Year 2022 to ₹1,341.83 million in Fiscal Year 2024. This strategic move aligns with the company's stated strength of "vertically integrated manufacturing competencies". This pivot is likely a contributing factor to the observed improvements in Gross and Operating EBITDA margins, as EPC services typically command higher profitability compared to pure product sales.

However, it also introduces increased operational complexity and a greater reliance on robust project execution capabilities. The significant decline in non-solar pump revenue, such as Non-Solar Submersible pumps dropping from 23.89% to 5.49%, indicates a deliberate de-emphasis or a natural decline in demand within these traditional segments, further solidifying the company's solar-centric strategy.

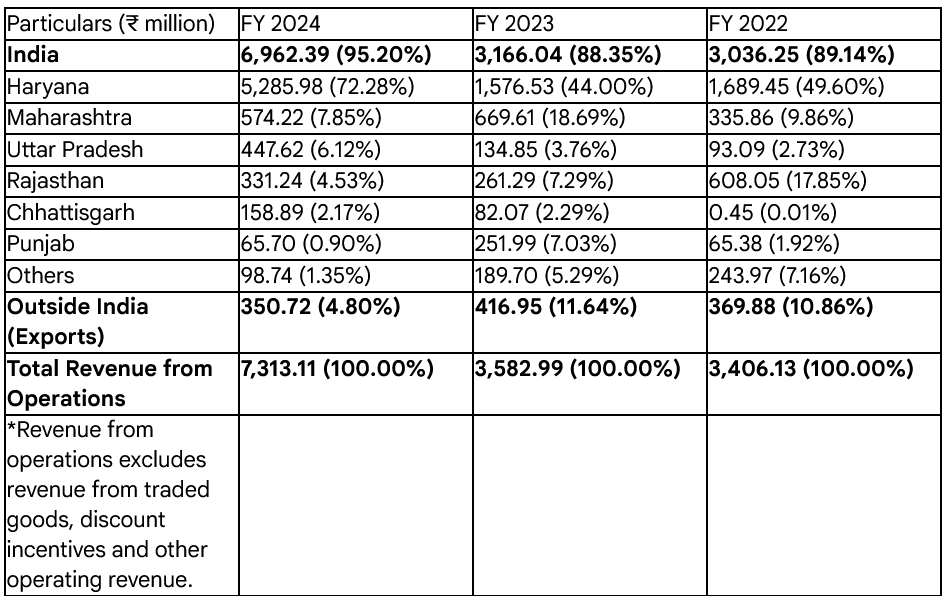

Geographical Revenue Bifurcation

Oswal Pumps maintains a strong domestic presence, particularly in key agricultural states, complemented by a growing international footprint

Despite the company's stated aim for a wider presence, the geographical revenue breakdown reveals a substantial concentration in Haryana, which accounted for 72.28% of domestic revenue in Fiscal Year 2024. This indicates a significant geographical concentration risk. While the company is expanding into other states, the impact of this diversification appears to be slower than the growth originating from Haryana, likely due to specific large-scale projects, such as those under the PM Kusum Scheme, within that state. This high concentration makes Oswal Pumps particularly susceptible to policy shifts, heightened competitive pressures, or adverse agricultural and economic conditions specific to Haryana. Therefore, the strategic imperative to expand into states like Maharashtra, Karnataka, and Madhya Pradesh is not merely an opportunity but a critical necessity for mitigating this risk and ensuring the company's long-term stability and diversified growth.

Between April 2021 and March 2024, the company successfully exported products to 17 countries across the Asia-Pacific, Middle East, and North Africa regions, including Australia, Egypt, Iraq, Italy, Lebanon, Libya, Nepal, Saudi Arabia, UAE, and Yemen.

Detailed Description of Manufacturing Facilities and Processes

Oswal Pumps operates two distinct manufacturing facilities, both located in Karnal, Haryana, and both running 24 hours a day, six days a week, with Sundays and national holidays as exceptions.

OPL Facility (Pumps and Electric Motors):

Commencement: Operations began in 2010. The facility spans a total land area of 41,076 square meters, with 39,159 square meters utilized and 23,940 square meters actively used for manufacturing activities as of March 31, 2024.

Installed Capacity (as of March 31, 2024): The facility has an annual installed capacity of 1,160.07 metric tonnes (MT) for stainless steel pumps, 2,123.05 MT for cast iron pumps, 1,314.72 MT for stainless steel motors, and 561.60 MT for cast iron motors.

Capacity Utilization (Fiscal 2024): Capacity utilization rates were 57.10% for stainless steel pumps, 73.10% for cast iron pumps, 44.90% for stainless steel motors, and 81.40% for cast iron motors.

Key Processes: The facility employs a range of sophisticated manufacturing processes, including Cast Iron (CI) Casting using automatic molding machines, Aluminum Die Casting for rotors with vertical and horizontal hydraulic pressure die casting machines, and Investment Casting for critical components like impellers and diffusers. Other processes include Electrical Stamping, Thrust Bearing production, Stainless Steel (SS) Pipe manufacturing, Plastic Injection Moulding, Winding Wire production, Cable Manufacturing, Automatic Winding, and an in-house Packaging unit.

Quality Control: The facility is equipped with four dedicated quality testing beds and advanced testing equipment, such as ring flow meters and digital volt amp watt meters, to ensure products meet stringent ISI and CE standards.

Certifications: The OPL facility holds ISO 9001:2015, ISO 45001:2018, and ISO 14001:2015 certifications.

Oswal Solar Structure Private Limited Facility (Solar Modules):

Commencement: Commercial production began on January 8, 2024. The facility occupies a total land area of 11,002 square meters, with 10,489 square meters utilized and 7,480 square meters dedicated to manufacturing.

Installed Capacity (as of March 31, 2024): The annual installed capacity for solar modules was 170 megawatts (MW).

Capacity Utilization (Fiscal 2024): The facility operated at a 15.23% capacity utilization rate.

Capacity Expansion: An additional 400 MW capacity has been installed and commissioned, with commercial production anticipated by the end of September 2024. The company has plans for a further 3,000 MW expansion.

Key Processes: Manufacturing processes include Non-Destructive Cell Cutting, Tabber & Stringer for automated cell welding, Auto-Bussing for interconnections, Electroluminescence (EL) Testing for microcrack detection, Lamination, Framing with aluminum structures, and Sun-simulator Testing.

Certifications: This facility also holds ISO 9001:2015, ISO 45001:2018, and ISO 14001:2015 certifications and is included in the ALMM list.

OPL's vertical integration is further strengthened by its associate company, Walso Solar Solution Private Limited, which specializes in manufacturing mounting structures and Balance of System (BOS) kits essential for Turnkey Solar Pumping Systems.

Current Operational Status and Market Footprint

The company maintains a robust distribution network in India, which expanded from 473 distributors in Fiscal Year 2022 to 636 distributors as of March 31, 2024. This extensive network facilitates broad reach to retail customers across the country. In March 2024, OPL introduced the 'Oswal Shoppe' concept, a strategic initiative to enhance market presence and strengthen relationships with retailers. As of the Draft Red Herring Prospectus date, there are 54 such shoppes, primarily concentrated in Haryana, Punjab, Uttar Pradesh, and Rajasthan.

Oswal Pumps serves both institutional customers, including notable entities like Tata Power Solar Systems Limited and Ecozen Solutions Private Limited, and various state entities under the PM Kusum Scheme. The company's international reach is demonstrated by its exports to 17 countries across Asia-Pacific, the Middle East, and North Africa between April 2021 and March 2024.

3. Growth Drivers, Challenges, and SWOT Analysis

A comprehensive evaluation of Oswal Pumps Limited necessitates a thorough understanding of its internal strengths and weaknesses, as well as the external opportunities and threats that shape its operating environment.

Strengths (Internal Capabilities & Advantages)

Leadership in PM Kusum Scheme: Oswal Pumps has demonstrated exceptional growth, emerging as the fastest-growing vertically integrated solar pump manufacturer in India, with a Compound Annual Growth Rate (CAGR) of 45.07% in revenue from Fiscal Year 2022 to Fiscal Year 2024. The company has strategically evolved from a traditional pump manufacturer to a diversified player in solar and grid-connected pumps and motors. This transformation has culminated in OPL becoming one of the largest suppliers of solar-powered agricultural pumps under the PM Kusum Scheme in Fiscal Years 2023 and 2024. As of August 31, 2024, the company had successfully executed orders for 26,270 Turnkey Solar Pumping Systems (TSPS) directly through the scheme in key agricultural states such as Haryana, Rajasthan, Uttar Pradesh, and Maharashtra. The increasing reliance on and success within the PM Kusum Scheme is evident, with revenue from this initiative (direct and indirect) constituting 85.72% in FY24, up from 69.74% in FY23 and 55.32% in FY22. This strong performance aligns with the broader Indian solar pump market's projected growth, which is expected to expand from ₹51.8 billion in FY24 to ₹218.2 billion by FY29, at a robust CAGR of 33.3%.

Extensive Vertical Integration: OPL's operations are characterized by deep vertical integration, encompassing the manufacturing of components for its pumps and the in-house production of solar modules. This is further bolstered by its associate company, Walso Solar Solutions, which specializes in mounting structures and Balance of System (BOS) kits. This integrated approach facilitates new product design and development, optimizes operational costs, and contributes to improved margins, as reflected in OPL's Operating EBITDA margin of 19.79% in FY24, which was the second highest among its peers. The company's end-to-end pump manufacturing capabilities include processes such as cast-iron casting, aluminum die casting, electrical grade stamping, and various molding techniques, supported by an in-house tool room for timely maintenance. The commencement of solar module manufacturing through Oswal Solar Structure Private Limited (OSSPL) in January 2023 further enhanced this backward integration.

Strong Engineering and Design Capabilities: A dedicated team of 15 employees, as of March 31, 2024, drives product design enhancements and cost-saving innovations. Notable examples include the optimization of submersible pump locking mechanisms and the reduction of non-return valve thickness through advanced manufacturing techniques. The team leverages sophisticated simulation software for computational fluid dynamics and seismic analysis, alongside industry-standard CAD/CAM tools like AutoCAD and SolidWorks, to ensure product quality and efficiency.

Comprehensive Product Portfolio: Oswal Pumps offers a broad spectrum of solar-powered and grid-connected submersible and monoblock pumps, electric motors, and solar modules under its 'Oswal' brand. This diverse portfolio caters to agricultural, residential, and industrial sectors, attracting new customers, expanding market reach, and mitigating business risks by reducing over-reliance on a single product or market segment. The products are available with varied specifications, including capacity, power, and voltage compatibility, for both domestic and international markets.

Extensive Distribution Network: The company's distribution network has expanded significantly, from 473 distributors in March 2022 to 636 distributors by March 2024. This robust network is a key differentiator, enabling OPL to effectively reach retail customers across India. The launch of the 'Oswal Shoppe' concept in March 2024 further strengthens market presence and retailer relationships, with 54 such exclusive retail points established as of the Draft Red Herring Prospectus date. OPL also serves institutional customers and has an international presence, exporting to 17 countries between April 2021 and March 2024.

Experienced Promoter and Senior Management Team: The company benefits from the extensive experience of its Chairman and Managing Director, Vivek Gupta, who possesses over 17 years of experience in the pump manufacturing industry. The leadership team, including Whole-time Directors Amulya Gupta (brand development) and Shivam Gupta (solar pumps business development), and independent directors with diverse expertise, has been instrumental in the company's growth and ability to capitalize on market opportunities.

Weaknesses (Internal Limitations)

Fluctuating Input Costs: The cost of materials consumed constitutes the majority of OPL's cost structure. Primary raw materials such as copper, stainless steel, pig iron, polypropylene, electrical grade sheets, EVA sheets, glass, and solar cells are subject to high price volatility influenced by global trade policies and economic conditions. The company's reliance on purchase orders rather than long-term agreements with suppliers exposes it to these fluctuations. An inability to effectively pass on increased raw material costs to customers could negatively impact margins, results of operations, and cash flows.

High Upfront Costs for Solar Solutions: Despite the long-term benefits, solar pumps entail higher initial investment compared to grid-connected alternatives, requiring capital for pumps, solar panels, controllers, and installation. This high upfront cost can deter adoption by certain customer segments, particularly lower and middle-class households, even with available subsidies.

Significant Working Capital Requirements: As a manufacturer and supplier to government entities, OPL incurs substantial upfront costs for raw materials, manufacturing, and distribution. Delays in subsidy payments from the government under schemes like PM-KUSUM can strain the company's liquidity and working capital position.

Reliance on Skilled Workforce: As an EPC player, Oswal Pumps requires a highly skilled workforce to maintain manufacturing quality standards. A shortage of qualified and experienced technical personnel can lead to production inefficiencies and potential quality control issues.

Increasing Competition: The market is becoming increasingly competitive, with more companies expanding their operations and pursuing backward and forward integration strategies, potentially intensifying competitive pressures on OPL.

Dependence on Top Customers: OPL's business is significantly concentrated among its top 10 customers, who contributed 79.50% of revenue from operations in FY24. The loss of any of these key customers could have a substantial adverse effect on the company's business, financial condition, and cash flows.

Reliance on Government Schemes with Expiry Dates: The company's sales are heavily supported by government policies and incentives, particularly the PM Kusum Scheme, which is scheduled to expire in December 2026. There is no guarantee of the scheme's extension, and any adverse changes or its termination could severely impact the business.

Leasehold Properties: OPL's manufacturing facilities and Registered and Corporate Office are situated on leased land. The inability to renew these leasehold rights or the loss of these properties could adversely affect business operations.

Auditor Observations: The statutory auditors have raised observations regarding the accounting software's audit trail, discrepancies in working capital returns filed with banks, and outstanding statutory dues. While the auditors did not find evidence of tampering, these observations indicate internal control weaknesses that warrant attention.

Opportunities (External Growth Avenues)

Growing Indian Pump Market: The Indian pump market, valued at ₹214.7 billion in FY24, is projected to reach ₹381.6 billion by FY29, growing at a CAGR of 12.2%. This growth is driven by urbanization, rapid industrialization, declining groundwater levels, and government initiatives aimed at improving water infrastructure.

High Growth in Agricultural Pumps: The agricultural pump sector is a key growth driver, expected to achieve the highest CAGR of 14.4% by FY29, constituting approximately 53% of the Indian pump industry. This growth is fueled by increasing adoption of solar pumps, demand for modern irrigation techniques, and continued government support.

Significant Potential in Indian Solar Pump Market: The Indian solar pump market, valued at ₹51.8 billion in FY24, is projected to reach ₹218.2 billion by FY29, with a robust CAGR of 33.3%. Government initiatives like PM-KUSUM, coupled with increasing energy efficiency awareness and cost savings, are primary drivers.

Untapped Market for Solar Pumps: A vast untapped market exists in India, with approximately 8 million farmers still relying on diesel-powered pumps and 114 million farmers lacking any access to pumps. The potential for replacing diesel pumps is estimated at ₹1,200 billion (USD 14.5 billion), and the market for providing pumps to farmers without access is around ₹2,400 billion (USD 29.1 billion).

Replacement Market for Pumps: The existing 21.6 million groundwater pumps in India, typically replaced every five years, offer substantial growth opportunities for solar-powered agricultural pumps. This replacement market is estimated at ₹65 billion in FY24 and is expected to reach ₹143 billion by FY29.

Growing Global Solar PV Market: The global PV solar market saw a 32% increase in installed capacity in 2023, driven by demand for cost-effective electricity, rising investments, and supportive government policies.

Export Opportunities due to Trade Dynamics: Trade disputes, particularly between China and the US, are creating significant export opportunities for Indian solar module producers. India's solar module exports surged 91% to USD 1.97 billion in FY24, with the USA being the primary destination. The US solar module market is projected to grow from USD 19 billion in 2023 to USD 38 billion in 2028, while the European market is expected to reach USD 37 billion by 2028.

Declining Solar Panel Costs: A 21% drop in module prices in the first five months of FY24, due to polysilicon oversupply, makes solar energy more cost-effective and boosts adoption.

Government Support for Solar Manufacturing: Initiatives like the Production Linked Incentive (PLI) Scheme and Basic Customs Duty (BCD) on imported solar components aim to bolster domestic manufacturing and reduce import reliance.

Growth in Electric Motor Market: The Indian electric motor market is estimated at USD 3.6 billion in FY24 and is projected to reach USD 1.1 billion by FY29, growing at a CAGR of 14.5%.

Increasing Demand for Industrial Pumps: The Indian industrial pump market is expected to grow at a CAGR of 10.5% by FY29, driven by industrialization, infrastructure development, and wastewater treatment regulations.

Threats (External Risks)

Expiration of Government Schemes: The PM Kusum Scheme, a significant revenue driver, is scheduled to expire in December 2026. The lack of assurance regarding its extension or any adverse changes to the scheme could severely impact OPL's business, financial condition, and cash flows.

Raw Material Price Volatility: Fluctuations in the prices of key raw materials like stainless steel, copper, and aluminum, driven by global trade policies and economic conditions, pose a continuous threat to production costs and margins if not effectively managed or passed on to customers.

Customer Concentration: The high dependence on a few top customers means that the loss of any one of them could significantly impair revenue and profitability.

Leasehold Property Risks: The company's reliance on leased manufacturing facilities and corporate offices introduces risks related to lease renewals, potential increases in rent, or the inability to secure new suitable locations, which could disrupt operations.

Regulatory Changes: Evolving laws, rules, and regulations in India could introduce new compliance requirements, potentially increasing operational costs or limiting business activities.

Intensifying Competition: The increasing number of companies expanding operations and integrating vertically in the pump and solar sectors could lead to heightened competition, impacting market share and pricing power.

Working Capital Management: Delays in government subsidy payments, coupled with the high upfront costs of manufacturing and distribution, could strain the company's working capital and liquidity.

Skilled Labor Shortage: A scarcity of qualified technical personnel required for high-quality manufacturing and EPC services could lead to production inefficiencies and quality control issues.

Oversupply in Solar Module Market: While OPL is expanding its solar module capacity, a potential oversupply in the broader market could force the company to reduce production volumes or lower prices, diminishing the benefits of expansion.

Unappraised Funding Requirements: The company's funding requirements and proposed deployment of Net Proceeds from the IPO have not been appraised by a bank or financial institution. This lack of external validation means that potential delays or cost overruns could adversely affect the business.

4. Future Growth Guidance and Management Commentary

Oswal Pumps' management has articulated a clear strategic roadmap aimed at sustaining its growth trajectory, enhancing operational efficiencies, and diversifying its market presence. These plans are underpinned by significant recent developments that reinforce the company's commitment to its long-term vision.

Strategic Initiatives for Future Growth

The management's strategic plans are multifaceted, focusing on deeper integration, automation, market expansion, and product diversification.

Backward Integration in Pump Manufacturing and Enhanced Automation: The company intends to further integrate its operations to optimize margins. This includes:

Integrating New Processes: Plans involve incorporating no-bake casting and aluminum heat sink die casting into manufacturing. No-bake casting offers advantages such as the ability to create complex profiles, lower production costs, and suitability for high-value components, while aluminum die casting provides lightweight, corrosion-resistant parts with superior thermal and electrical conductivity.

In-house Production of VFDs and Single-Phase Controllers: Currently procured from external vendors, Variable Frequency Drives (VFDs) are in the trial phase for in-house development, with commercial production slated to commence upon successful conclusion of trials. This move is expected to improve profitability. Similarly, the company plans to internally produce single-phase AC voltage controllers.

Automating Manufacturing Processes: OPL aims to automate press, welding, and CNC operations through the implementation of robotic systems and automatic quality checks. This automation is projected to reduce labor costs, increase production efficiency, enhance product quality, improve traceability, and optimize space utilization.

Strategic Acquisitions: The company may pursue inorganic growth opportunities through acquisitions to bolster its technological capabilities and enhance the automation and IT interfaces of its products.

Focus on Government Schemes and Maintaining Leadership Position: Oswal Pumps plans to leverage its manufacturing capabilities to capitalize on the ongoing growth opportunities presented by the PM Kusum Scheme. Despite the scheme's target of 1.40 million standalone solar pumps, only 0.33 million have been installed as of April 30, 2024, indicating a substantial untapped market. The company intends to expand its operations into states with high potential, such as Maharashtra, Karnataka, and Madhya Pradesh, by actively participating in bidding processes and expanding its distributor network.

Direct Sales to Farmers: Recognizing that some farmers may prefer immediate solutions, Oswal Pumps aims to utilize its extensive distribution network to directly offer solar-powered agricultural pumps, allowing farmers to benefit from immediate cost savings without waiting for government subsidies.

Increase Manufacturing Capacity for Solar Modules and Backward Integration: The company has ambitious plans to expand its solar module manufacturing capacity and deepen its backward integration in the solar module value chain:

Backward Integration in Solar Modules: This includes the in-house production of aluminum extrusion frames, ethylene-vinyl acetate (EVA), junction box back sheets, and on-grid inverters. This strategy is expected to provide greater control over the supply chain, improve product quality, and optimize costs.

Capacity Expansion: As of March 31, 2024, the solar module capacity was 170 MW. An additional 400 MW capacity has been commissioned, with commercial production expected by the end of September 2024. The company intends to further increase this capacity by 3,000 MW to meet future demand in both Indian and global markets.

Market Diversification for Solar Modules: OPL plans to supply solar modules to a broader range of third-party entities, including existing and new distributors, participants in the PM Kusum Scheme, original equipment manufacturers (OEMs), government entities, and private large rooftop and ground-mounting projects. Furthermore, the company aims to export solar modules to the United States and Europe, capitalizing on the substantial market sizes in these regions.

Introduce New Products in Industrial Pumps and Electric Motors: To capitalize on rising demand, Oswal Pumps plans to diversify its product portfolio by introducing a range of industrial pumps, including helical rotor pumps, progressive cavity pumps (PCP), industrial centrifugal pumps, inline pumps, pressure pumps, reciprocating pumps, and chemical pumps. The company also intends to introduce vibrant electric motors, primarily targeting the construction, food, and flour industries.

Increase Presence in Select Geographies in India and Grow Exports: The company aims to enhance its domestic presence by expanding its distributor network, particularly in states like Chhattisgarh, Karnataka, Assam, Kerala, Andhra Pradesh, Telangana, Tamil Nadu, and Gujarat. In parallel, OPL plans to increase exports of its solar and non-solar pumps and electric motors to existing international markets (e.g., Australia, Egypt, Iraq, Italy, Lebanon, Libya, Nepal, Saudi Arabia, UAE, Yemen) and explore new geographies such as Spain, South Africa, Sri Lanka, and Australia. A specific focus is placed on exporting solar modules to the United States. The 'Oswal Shoppe' concept will also be expanded across various states to strengthen relationships with distributors and retailers, thereby enhancing brand visibility and driving revenue growth.

Significant Developments After March 31, 2024

Several key developments have occurred since the last balance sheet date, indicating active progression of the company's strategic plans:

Change in Shareholding of Subsidiaries: Oswal Solar Structure Private Limited and Oswal Green Industries Private Limited became wholly-owned subsidiaries of Oswal Pumps Limited, effective July 24, 2024.

Enhancement of Existing Limits and New Credit Facilities: The company secured new credit limits of ₹605 million and extended existing credit limits by ₹612.5 million from State Bank of India, Citi Bank N.A., and YES Bank, bolstering its financial flexibility.

Purchase of Land in Sonipat: Oswal Pumps acquired new land in Sonipat for warehousing purposes, supporting its logistical and expansion needs.

Capacity Expansion: Oswal Solar Structure Private Limited initiated an increase in its solar module manufacturing capacity from 200 MW to 600 MW, a crucial step towards meeting future demand.

Investment in Associate: Oswal Pumps acquired a 38.50% stake in Walso Solar Solution Private Limited, making it an associate company and further integrating its supply chain.

Shares Split: The Board of Directors and Shareholders approved the sub-division of each equity share from a face value of ₹10 to ₹1, effective August 29, 2024, enhancing liquidity and accessibility of shares.

Bonus Issue: A bonus issue of 40,963,300 equity shares (₹1 face value each) was approved and allotted on August 31, 2024, in the proportion of 7 equity shares for every 10 held, indicating confidence in future profitability and rewarding shareholders.

ESOP Scheme: The "Oswal Pumps Employee Stock Option Plan – 2024" was adopted, effective September 2, 2024, aligning employee incentives with company performance.

These strategic initiatives and recent developments collectively demonstrate management's proactive approach to capitalizing on market opportunities, enhancing operational capabilities, and addressing potential challenges. The focus on vertical integration and capacity expansion, particularly in the solar segment, positions the company to benefit from the growing demand for renewable energy solutions in agriculture and other sectors.

5. Financials: Breakdown and Growth Drivers

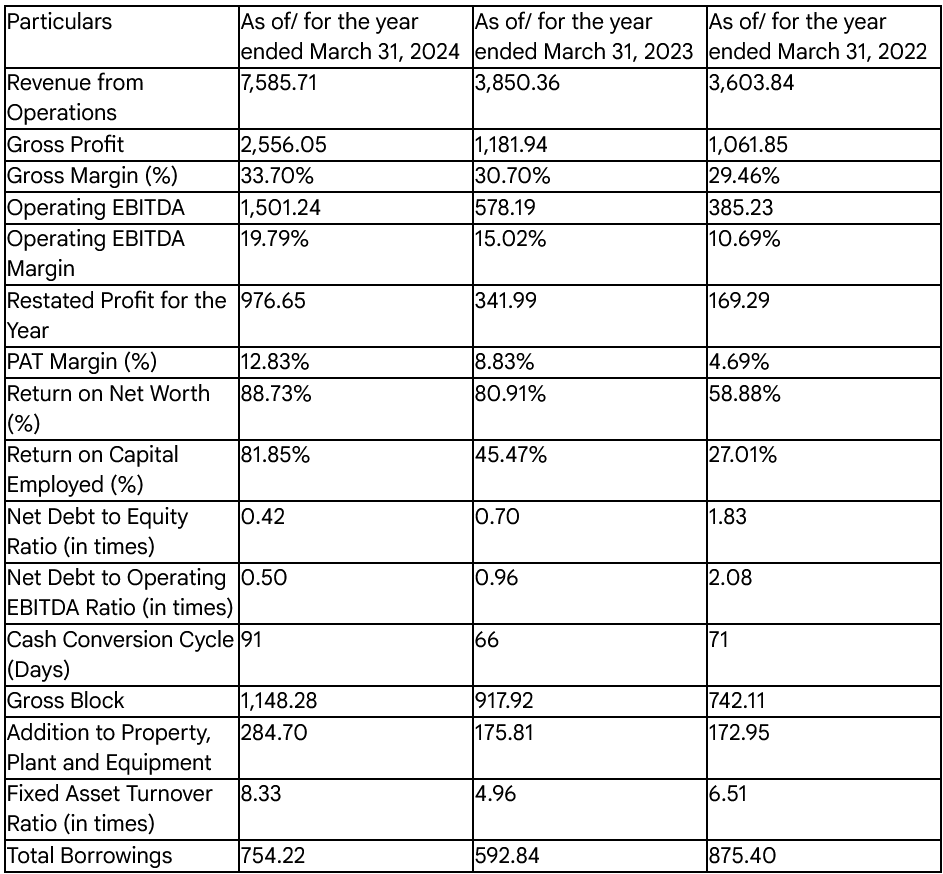

A detailed examination of Oswal Pumps Limited's financial performance over the last three fiscal years (FY2022, FY2023, and FY2024) reveals a strong growth trajectory and improving operational efficiency. The analysis is based on the Restated Consolidated Financial Information and Key Performance Indicators.

Summary of Restated Consolidated Financial Information (All amounts in ₹ million, except per share data):

Restated Consolidated Statement of Profit and Loss (All amounts in ₹ million, unless otherwise stated):

Key Performance Indicators (All amounts in ₹ million, unless otherwise stated):

Drivers of Revenue and Margin Growth

Revenue Growth:

Oswal Pumps Limited has demonstrated remarkable top-line expansion, with revenue from operations nearly doubling from Fiscal Year 2023 to Fiscal Year 2024, representing a 97.01% increase. This significant growth is primarily attributable to a substantial increase in the supply of Turnkey Solar Pumping Systems (TSPS) directly under the PM Kusum Scheme, alongside increased sales to institutional customers. The strategic shift towards providing comprehensive TSPS solutions, which includes installation and commissioning services, has allowed the company to capture a larger share of the value chain, driving substantial revenue growth in this segment. The expansion of the distribution network, which grew from 473 distributors in FY22 to 636 in FY24, has also contributed to broader market penetration and increased sales volumes. Additionally, the introduction of the 'Oswal Shoppe' concept in March 2024 is aimed at further bolstering market presence and driving future revenue growth through enhanced retailer relationships.

Margin Changes:

The company has exhibited improving profitability margins over the three fiscal years.

Gross Profit and Gross Margin: Gross profit has consistently increased, and the gross margin percentage has shown an upward trend, rising from 29.46% in FY22 to 33.70% in FY24. This improvement indicates enhanced efficiency in managing the cost of goods sold. The declining trend in the cost of goods sold as a percentage of revenue from operations, from 70.54% in FY22 to 66.30% in FY24, is a key factor contributing to this margin expansion. This improvement is largely attributed to the increasing revenue contribution from the supply of the entire solar pump and installation package directly under the PM Kusum Scheme, which likely offers better margins than standalone product sales.

Operating EBITDA and Operating EBITDA Margin: Both Operating EBITDA and its margin have significantly improved, with the margin increasing from 10.69% in FY22 to 19.79% in FY24. This substantial increase reflects enhanced operational efficiency and improved profitability from core business activities.

PAT Margin: The Profit After Tax (PAT) margin has also shown a healthy increase, from 4.69% in FY22 to 12.83% in FY24. This indicates a stronger bottom line, driven by both top-line growth and improved cost management.

While overall margins have improved, certain expense categories have seen increases:

Cost of Materials Consumed: This remains the most significant component of total expenses, representing 67.47% of total revenue from operations in FY24. While the percentage has decreased from 72.19% in FY22, fluctuations in raw material prices (e.g., copper, stainless steel, solar cells) remain a key factor influencing margins, particularly if increases cannot be fully passed on to customers.

Employee Benefits Expense: This expense increased by 44.48% from ₹293.49 million in FY23 to ₹424.02 million in FY24. This rise is primarily due to an increase in salaries, wages, and bonuses, driven by an expansion in the employee base from 1,673 to 1,851 and salary increments for existing personnel.

Finance Costs: Finance costs saw a significant increase of 142.55% from ₹59.01 million in FY23 to ₹143.13 million in FY24. This was mainly due to higher interest costs related to channel financing and bank borrowings, as well as an increase in finance corporate guarantee obligations.

Depreciation and Amortization: These expenses increased by 10.88% from ₹77.53 million in FY23 to ₹85.97 million in FY24, primarily due to an increase in the gross block of property, plant, and equipment, reflecting ongoing investments in manufacturing capabilities.

Other Expenses: Other expenses surged by 103.31% from ₹310.26 million in FY23 to ₹630.79 million in FY24. This increase was driven by higher expenses for installation and commissioning of solar pumps, advertisement and business promotion activities, communication costs, provision for expected credit loss, and miscellaneous expenses.

Despite these increases in specific expense categories, the overall improvement in gross margins and operational efficiencies, particularly from the growing TSPS segment, has translated into robust profitability growth for Oswal Pumps Limited.

6. Financial Red Flags

A thorough examination of Oswal Pumps Limited's financial integrity requires a close look at auditor observations, contingent liabilities, and related party transactions. While the provided information does not explicitly categorize "financial red flags," certain points warrant careful consideration by an investor.

Auditor Observations

The statutory auditors of Oswal Pumps Limited and its subsidiaries (Oswal Solar Structure Private Limited and Oswal Green Industries Private Limited) have highlighted several observations, primarily concerning accounting software and statutory compliance.

Accounting Software Audit Trail: For all three entities, the accounting software (specifically Microsoft Navision ERP) used for maintaining books of accounts had an audit trail (edit log) feature. However, this feature was not enabled at the database level throughout the year to log direct data changes. Furthermore, the audit trail was not enabled for the period of April 1, 2023, to April 2, 2023. For certain transaction categories, even when enabled, the audit trail did not capture the nature of changes made. While the auditors did not find instances of tampering, these limitations in the audit trail system represent a weakness in internal controls over financial reporting, potentially affecting the complete traceability of transactions and data alterations. Such a deficiency, while not necessarily indicative of malfeasance, introduces a degree of risk regarding data integrity and the robustness of financial records.

Working Capital Limits and Quarterly Returns: For Oswal Pumps Limited, the quarterly returns/statements submitted to banks for working capital limits exceeding ₹50 million were not consistently in agreement with the books of accounts for certain periods. For example, as of March 31, 2023, there were differences in Trade Receivable (₹24.57 million) and Trade Payable (₹27.68 million). As of December 31, 2023, a difference of ₹92.82 million was noted in Trade Payable. Similar discrepancies were observed for Oswal Solar Structure Private Limited, with a difference of ₹179.32 million in Trade Payable as of December 31, 2023. The stated reasons for these differences, such as "Periodic book closure entries" or "Statements are submitted having different date instead of March 31, 2023/2022," suggest reconciliation issues or timing differences. While common in practice, consistent discrepancies can indicate a lack of robust financial reconciliation processes or potential operational inefficiencies that could impact liquidity management and lender relations.

Undisputed Statutory Dues: As of March 31, 2024, Oswal Pumps Limited had undisputed outstanding statutory dues of ₹0.09 million for Provident Fund and ₹0.09 million for Employees State Insurance that were in arrears for more than six months from their due dates. Additionally, an advance tax of ₹4.58 million was an undisputed outstanding statutory due in arrears for more than six months as of the same date. While the amounts are small in relation to the company's overall financials, consistent delays in paying statutory dues, even minor ones, can signal administrative inefficiencies or, in a worst-case scenario, cash flow pressures.

Disputed Statutory Dues: Oswal Pumps Limited faces a disputed GST amount of ₹13.28 million related to FY 2019-20, currently pending at the High Court Chandigarh. Previous fiscal years also showed disputed Income Tax and TDS dues. The presence of disputed statutory dues is not uncommon for businesses, but the ongoing nature of these disputes and their resolution timeline should be monitored, as they could result in financial outflow if resolved unfavorably.

Cash Losses in Subsidiary: Oswal Green Industries Private Limited, a subsidiary, incurred cash losses of ₹0.06 million in Fiscal Year 2024. While the amount is minimal, and the subsidiary did not incur cash losses in the immediately preceding year, any cash loss in a subsidiary warrants attention to understand its operational viability and potential drain on consolidated resources, especially if it is a recurring issue.

Contingent Liabilities and Commitments

As of March 31, 2024, Oswal Pumps has several contingent liabilities and commitments that are not yet recognized on the balance sheet but could impact future financial performance:

Claims Against the Company Not Acknowledged as Debts:

Demands related to GST amount to ₹38.16 million, of which ₹24.88 million has been deposited under protest.

Demands related to Labour laws and others total ₹6.81 million.

Non-compliance with Companies Act, 2013: The company did not comply with Section 149(1)(b) of the Companies Act, 2013, regarding the appointment of a woman director up to March 31, 2024. An application for compounding the offense has been submitted and is pending.

Commitments:

Estimated Capital Expenditure Contracts: There are estimated contracts remaining to be executed on Capital Account (net of advances) totaling ₹34.36 million. This represents future cash outflows for capital investments.

Export Obligation under EPCG Scheme: A balance export obligation for importing capital equipment under the EPCG scheme amounts to ₹375.56 million. While management expects to fulfill this obligation, failure to do so could result in penalties or duties.

Related Party Transactions

Oswal Pumps engages in various transactions with related parties in the ordinary course of business, as detailed in the financial statements. These transactions involve the holding company, subsidiaries, key management personnel (KMP), their relatives, and entities with significant influence over the holding company.

Key Categories of Transactions (FY2022-FY2024):

Loans Taken and Repaid: The company has a history of taking and repaying loans from KMP and their relatives (e.g., Mr. Vivek Gupta, Mr. Amulya Gupta, Mr. Padam Sain Gupta, Mr. Shivam Gupta, and various HUFs). For instance, in FY24, Oswal Pumps Limited took ₹30.48 million from Mr. Vivek Gupta and repaid ₹50.23 million to him. Oswal Solar also took loans from and repaid loans to KMP.

Interest Expenses/Income on Loans: Interest is paid on these related-party loans.

Advances for Salary/Loans: Advances against salary were given to and refunded by relatives of KMP.

Equity Share Transactions: Issuance and purchase of equity shares of the subsidiary (Oswal Solar Structure Private Limited) involved KMP and their relatives.

Lease/Rent Payments: Rent is paid to KMP for leased properties (e.g., Mr. Vivek Gupta, Mr. Amulya Gupta).

Corporate Guarantees: Shorya Trading Company Private Limited, the holding company, provides corporate guarantees for borrowings, incurring finance corporate guarantee obligation expenses.1 Personal guarantees are also provided by directors for loans.

Purchase and Sale of Goods: Transactions include purchases from Solar Solution India and Solar Structure India, and sales to Solar Solution India.

Remuneration to KMP and Relatives: Compensation is paid to KMP and their relatives, including Mr. Vivek Gupta, Mr. Amulya Gupta, Mr. Padam Sain Gupta, Mr. Shivam Gupta, Mrs. Radhika Gupta, and Mrs. Vrinda Garg.

Closing Balances (as of March 31, 2024): Significant closing balances of interest payable, lease/rent payable, and loans payable to KMP and their relatives persist.

7. Concluding Remarks

Oswal Pumps Limited presents a compelling case for growth, driven by its strategic pivot towards solar pumping solutions and its strong positioning within government-backed initiatives. The company's vertically integrated manufacturing capabilities, robust engineering, and expanding distribution network underscore its operational strengths. However, a discerning investor must also weigh these positives against identified financial and operational risks.

The company's financial performance over the past three fiscal years has been impressive, characterized by a near doubling of revenue from operations from FY23 to FY24, and significant improvements in profitability metrics such as Gross Margin, Operating EBITDA Margin, and PAT Margin. This growth is largely attributable to the successful shift towards Turnkey Solar Pumping Systems (TSPS), which now constitutes the overwhelming majority of revenue, particularly under the PM Kusum Scheme. The reduction in Net Debt to Equity and Net Debt to Operating EBITDA ratios also indicates improving financial health and reduced leverage.

The management's strategic plans for future growth are well-defined and align with market opportunities. These include further backward integration in both pump and solar module manufacturing, significant capacity expansion for solar modules (an additional 3,000 MW planned), diversification into new industrial pump and electric motor categories, and aggressive geographical expansion within India and internationally. Recent developments, such as the commissioning of additional solar module capacity and the acquisition of land for warehousing, demonstrate tangible progress on these strategic fronts.

However, certain aspects warrant caution. The high revenue concentration in the agricultural sector (over 96% in FY24) and specifically in the state of Haryana (over 72% of domestic revenue in FY24) exposes the company to significant sectoral and geographical risks. This concentration is further amplified by the substantial reliance on the PM Kusum Scheme, which is set to expire in December 2026. While the company is actively pursuing diversification and expansion into other states, the success of these initiatives will be critical in mitigating this dependence. Furthermore, the auditor observations regarding accounting software audit trails and discrepancies in working capital returns, though not deemed material by the auditors, point to areas where internal financial controls could be strengthened. The extensive network of related-party transactions, while stated to be at arm's length, requires continuous monitoring to ensure transparency and protect minority shareholder interests.

Whether this business fits the 20% growth criteria?

Based on the available data and strategic outlook, Oswal Pumps Limited demonstrates a strong potential to meet the 20% earnings growth criteria over the next few years.

Historical Growth Trajectory: The company's Restated Profit for the Year has grown from ₹169.29 million in FY22 to ₹341.99 million in FY23, and further to ₹976.65 million in FY24. This represents a compounded annual growth rate (CAGR) of approximately 139% from FY22 to FY24. While such a high historical growth rate may not be sustainable indefinitely, it provides a strong foundation.

Market Tailwinds: The Indian solar pump market is projected to grow at a CAGR of 33.3% from ₹51.8 billion in FY24 to ₹218.2 billion by FY29. The broader Indian pump market is also expected to grow at 12.2% CAGR, with agricultural pumps leading at 14.4%. The significant untapped market for solar pumps in India (millions of farmers without access or using diesel pumps) presents a massive opportunity.

Strategic Initiatives: The planned solar module capacity expansion by an additional 3,000 MW, coupled with backward integration, positions the company to capture a larger share of this growing market. The diversification into industrial pumps and electric motors, markets also experiencing significant growth, provides additional avenues for revenue expansion beyond the core agricultural solar pump segment. The aggressive expansion of the distribution network and the 'Oswal Shoppe' concept will further drive sales volumes.

The company's ability to maintain its leadership in the PM Kusum Scheme while simultaneously expanding into new geographies and product categories, and successfully executing its capacity expansion and backward integration plans, will be crucial. The primary risk to sustaining this growth rate is the potential non-extension or adverse changes to the PM Kusum Scheme post-2026, which currently accounts for a substantial portion of revenue. However, management's proactive strategies to diversify revenue streams and market presence are designed to mitigate this very risk.

Given the substantial market opportunities, the company's proven execution capabilities in scaling its solar business rapidly, and its clear strategic roadmap for expansion and integration, it is reasonable to conclude that Oswal Pumps Limited possesses the fundamental drivers and strategic intent to achieve and potentially exceed a 20% earnings growth rate over the next few years. The key will be diligent execution of its diversification strategy and prudent management of its working capital and raw material costs.